Will My Roth IRA Conversion Be Penalty-Free?

Roth IRA conversions are among the most powerful—and most misunderstood—tax-planning tools available to high earners.

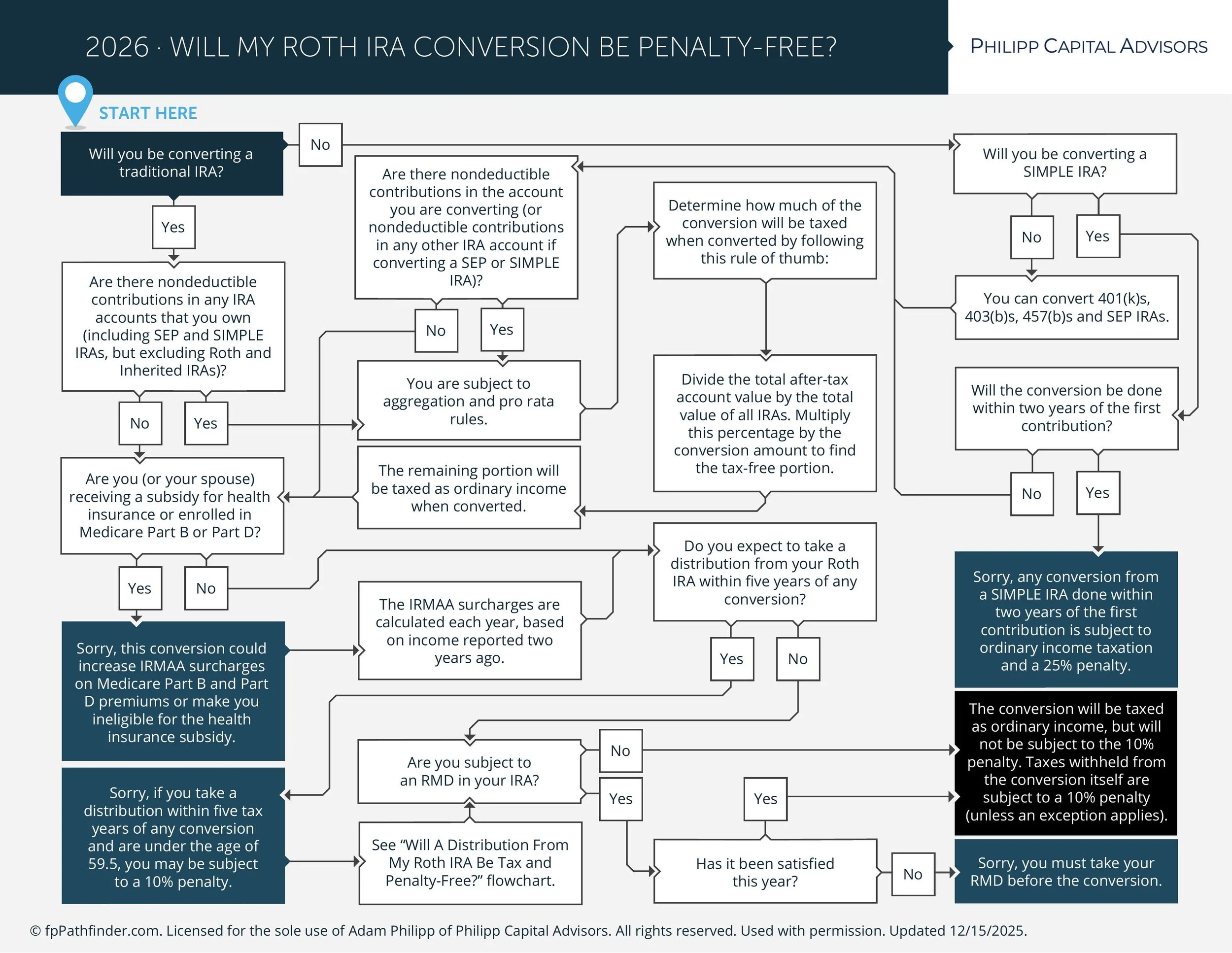

The concept is straightforward: convert pre-tax retirement money (traditional IRA, 401(k)) into a Roth IRA, pay taxes on the conversion now, and enjoy tax-free growth and withdrawals later.

Simple in theory. Messy in practice.

The rules governing Roth conversions involve a maze of exceptions, aggregation requirements, pro-rata calculations, and penalty triggers that can turn a smart tax move into an expensive mistake. Most people know conversions are taxable. Fewer realize they can also be penalized if they don’t navigate the rules correctly.

This week’s flowchart walks you through the decision tree: Will your Roth IRA conversion be penalty-free? It covers the critical questions most people miss: SIMPLE IRA timing rules, RMD requirements, the pro-rata trap, IRMAA surcharges, and the five-year rule that catches people who convert and then need the money too soon.

If you're considering a Roth conversion—or if your CPA suggested one and you're not entirely sure what you’re signing up for—this chart maps the path from “should I convert?” to “how do I do this without triggering penalties I didn't know existed?”